From a regional perspective, in September, the sales volume of Volvo Cars in Europe was 25,489, a year-on-year increase of 32%; Among them, the sales of Recharge series models in Europe increased to 13,599, accounting for 53% of Volvo Car’s sales in Europe. In the American market, the sales volume of Volvo cars increased by 65% compared with the same period of last year, reaching 10,946 vehicles; Among them, the proportion of Recharge series models is 28%. Sales of Volvo Cars in China increased by 4% year-on-year to 15,460 vehicles, among which sales of Recharge series vehicles in China increased by 20% year-on-year.

标签: 南京品茶交流

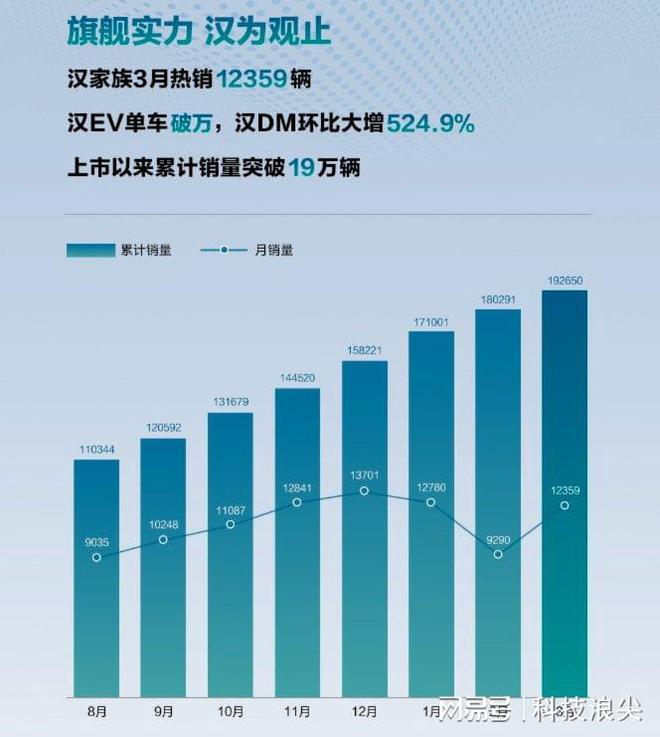

BYD Han EV’s monthly sales exceeded 10,000, and the fuel vehicle was officially discontinued.

BYD announced on April 3, 2022 that it officially became the first car company in the world to stop producing fuel vehicles. It is worth mentioning that at last year’s COP26 climate conference, many car companies around the world jointly stated that the production of fossil fuel vehicles will be gradually stopped worldwide by 2040. Among them are BYD, Ford, General Motors, Jaguar Land Rover, Mercedes-Benz, Volvo and other enterprises. BYD is the only China car company that is a signatory. At the same time, BYD has also become the fastest one to fulfill its promise.

In addition to the heavy news that fuel vehicles stopped production, BYD also announced its sales results in March. It is reported that BYD sold more than 100,000 vehicles in March, and the sales volume of BYD Han alone broke Wanda to 12,359 vehicles, an increase of 33% from the previous month. Among them, the sales volume of Han EV bicycles exceeded 10,000, reaching 10,178; Han DM sales increased by 524.9% month-on-month. By March, 2022, the cumulative sales volume of BYD Han family had exceeded 190,000, ranking firmly in the Top1 of China brand medium and large cars. BYD can be said to be a new energy leader.

At present, it is a global consensus to achieve peak carbon dioxide emissions and carbon neutrality, and emission standards are being tightened around the world. BYD is also actively following the national "double carbon" strategic goal to promote the green and low-carbon development of the automobile industry. BYD’s super hybrid vehicles have completely surpassed fuel vehicles in terms of performance and fuel consumption. Take BYD’s latest Han DM-i/DM-p as an example. It is equipped with BYD’s blade battery, DiSus-C intelligent electronically controlled active suspension, DiLink 4.0(5G) intelligent network connection system, DiPilot intelligent driver assistance system, maximum 80kW safe boost DC fast charging and high-efficiency heat pump air conditioning in wide temperature range.

Among them, the acceleration of the Han DM-p model can reach an astonishing 3.7s per 100 km, while the pure battery life of the Han DM-p model can reach 242KM, the fuel consumption is 4.2L/100KM, and the comprehensive battery life is 1300KM. Commuting to and from work in urban areas is completely pure electricity to save money. Even when you go back to your hometown and go on road trip on holidays, the fuel consumption is lower than that of traditional fuel vehicles. In this way, for most consumers, with DM-i/DM-p models, there is no point in buying traditional fuel vehicles at all.

Due to the mixed production of PHEV and fuel vehicles, from the perspective of development, stopping the production of fuel vehicles now will not only have no commercial losses, but also transfer the production capacity to new energy vehicles. It is obviously a win-win situation for DM-i models to be delivered to consumers faster. From the brand point of view, it can be upgraded from a brand in the era of fuel vehicles to a completely pure new energy vehicle enterprise, and from the brand image point of view, it will become more vigorous.

New energy vehicles are the biggest catch for our national automobile industry to overtake in corners. It is precisely because BYD has the determination to burn its bridges that we have the opportunity to catch up with or even surpass the automobile industries in Germany, Japan and the United States. Whoever is unwilling to change will be eliminated by the times. Other traditional fuel vehicle manufacturers also understand this truth, but most of them are reluctant to part with the existing fuel vehicle market.

To sum up, BYD, as the "first brother" of the current domestic new energy vehicle enterprises. It is a very bold and decisive decision to establish the brand tonality of pure electric vehicles. After unloading the "historical burden" of fuel vehicles, BYD’s pure electric vehicles and DM-i super hybrid "walk on two legs" and have infinite potential in the future.

Real estate weekly and first-tier cities are expected to lead the real estate market to stabilize and recover.

Focus on new signals of real estate market

editorial comment/note

Recently, many new signals have appeared in the real estate market. According to the data of the National Bureau of Statistics, the signal that the real estate market in first-tier cities stabilized and rebounded in September was obvious. It is worth noting that the central and local policies to stabilize the property market continue to increase, the market is clearing, and normal investment demand has rebounded. In first-tier cities, the policy of "recognizing housing but not loans" is superimposed on the traditional "golden nine and silver ten", and some positive changes have taken place in the real estate market in first-and second-tier cities.

Half-monthly talk on property market

Image source/Xinhua News Agency

■ China Economic Times reporter Xia jinbiao

In the past two months, various support policies for the real estate market have been implemented nationwide, and the policy effects are gradually emerging. The real estate market is showing signs of recovery-the real estate market in first-tier cities is the first to recover.

According to the housing price data of 70 cities published by the National Bureau of Statistics in September, the sales price of new houses in first-tier cities turned flat from 0.2% in August, with Beijing and Shanghai rising by 0.4% and 0.5% respectively, with Shanghai leading the country.

Since the end of August, the easing policies of the real estate market in many places have been continuously released. In particular, the four first-tier cities in the north, Guangzhou and Shenzhen have successively implemented the policy of "recognizing houses but not loans", which has obviously boosted the real estate market. Take Shanghai, which led the rise in September, as an example. Following the announcement of the implementation of commercial loans on September 1, on October 17, Shanghai announced the optimization of the criteria for determining the number of housing provident fund loans. If Shanghai has no housing, no provident fund loans in the country or the first provident fund loans have been settled, it will be recognized as the first set of housing … The policy has been continuously exerted, boosting the Shanghai real estate market.

From the perspective of the second-hand housing market, the price of second-hand housing rose by four cities in September, an increase of one city compared with August. First-tier cities turned up for the first time after falling for four consecutive months, with an increase of 0.2%. Among them, Beijing led the national second-hand housing market with an increase of 0.7%; Followed by Shanghai, the price of second-hand housing rose by 0.6%.

Some insiders believe that the price of second-hand houses in Beijing and Shanghai has increased month-on-month, mainly due to the strict implementation of the policy of "recognizing houses and recognizing loans" in Beijing and Shanghai. After the implementation of "recognizing houses but not recognizing loans", the demand potential released is relatively large, especially in Beijing and Shanghai. There are many old second-hand houses, and there is great potential for improved demand, and the activity of second-hand houses has increased.

It should be pointed out that although first-tier cities take the lead in recovery, this recovery is still unstable, and there are still divisions within first-tier cities. The prices of new houses in Guangzhou and Shenzhen continued to fall, with a month-on-month decrease of 0.6% and 0.5% respectively, and a year-on-year decrease of 1.7% and 3%. The price of second-hand houses in Guangzhou decreased by 0.7% month-on-month, while the price of second-hand houses in Shenzhen was flat.

In addition, although the sales price of commercial housing in second-and third-tier cities has increased and decreased year-on-year, the chain is still declining. From the ring comparison, in September, the sales price of new commercial housing in second-tier cities decreased by 0.3% from the previous month, and the decline rate was 0.1 percentage points higher than that of the previous month. Second-hand housing decreased by 0.5% month-on-month, the same as last month. The sales price of new commercial housing in third-tier cities decreased by 0.3% month-on-month, and the decline rate narrowed by 0.1 percentage point from last month; Second-hand housing decreased by 0.5% month-on-month, and the decline rate was 0.1 percentage point higher than that of last month.

At present, the risk release of the real estate supply side continues, and residents’ income and expectations need to be further improved, which has affected the stabilization of the real estate market in second-and third-tier cities to a certain extent, resulting in the decline in house prices in second-and third-tier cities. In addition, the recovery of first-tier cities brought by optimizing real estate policies needs to be further stabilized.

Due to the implementation of policies such as "recognizing houses but not loans", the demand for housing replacement in first-tier cities has been released, which has led to a significant increase in the number of second-hand houses listed in first-tier cities. Under the background of a large increase in supply, the prices of second-hand houses in first-tier cities are still in a downward channel in the short term.

Some insiders believe that whether it is just needed or improving demand, residents usually "buy up and not buy down". At present, consumers’ confidence in housing prices and the market is weak, and they are more cautious and slow to enter the market. In this regard, it is necessary to further optimize the real estate policy, "stabilize housing prices" and "stabilize expectations" and promote the repair of the real estate market.

In the short term, the real estate market is still facing adjustment pressure. However, in the medium and long term, the urbanization rate of permanent residents in China is 65.2%, and the urbanization rate of registered population is only 47.7%, so there is still much room for improvement in urbanization. In addition, although the total number of houses in China has reached about 40 billion square meters, the houses are mainly small and medium-sized units with great improvement potential.

The market expects that the policy is expected to continue to be optimized around stabilizing housing price expectations, activating the replacement chain, and lowering the threshold for reasonable housing demand. In particular, with the further liberalization of policies such as purchase restriction in first-tier cities, hot cities will enter a more solid market recovery stage, which is expected to lead the real estate market out of the bottom area and stabilize and recover.

The copyright of this WeChat official account belongs to China Economic Times. If you reprint or quote the contents of this article, you must obtain permission, and indicate that it was transferred from China Economic Times.

Reporting/feedback